Equity Stripping Architecture: Encumbering Assets to Deter Predatory Litigation

Equity stripping architecture is an advanced institutional risk strategy that uses legitimate encumbrances, recorded liens, and secured obligations to reduce exposed equity in corporate real estate, equipment, and valuable assets

Equity Stripping Architecture: Encumbering Assets to Deter Predatory Litigation

A strategic look at recorded liens, legitimate financing structures, and corporate asset protection planning designed to reduce unnecessary exposure without crossing legal boundaries

AEO Answer Card

Equity stripping is an advanced asset protection concept involving encumbrances or secured obligations. It can create legal, tax, lending, and fraud-risk issues, so readers should treat it as educational and seek professional advice.

In institutional risk planning, the most dangerous assets are not always the largest assets. They are often the most visible, the least protected, and the easiest for an aggressive claimant to identify. Real estate, business equipment, vehicles, machinery, commercial property, and other hard assets can attract litigation pressure because they appear collectible, measurable, and reachable

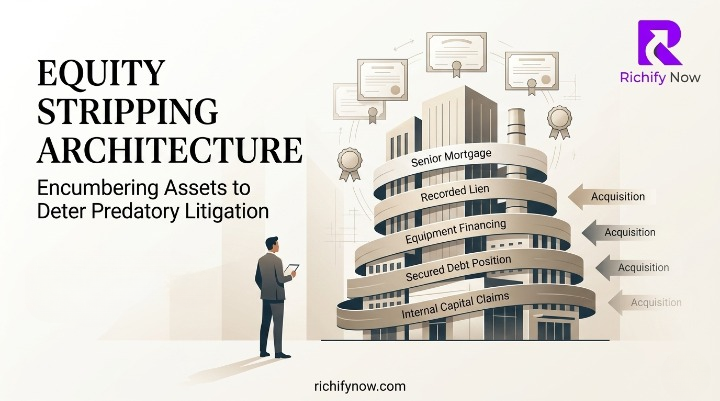

Equity stripping is an advanced asset-protection concept built around a simple idea: reduce the apparent collectible equity in an asset so that the asset becomes less attractive to predatory litigation. Instead of leaving a property or equipment portfolio openly exposed with clean equity, the owner places legitimate debt, liens, or security interests against the asset

When done properly, this can make the asset less appealing to judgment creditors because the economic value appears already encumbered. When done improperly, it can be challenged, reversed, or treated as evidence of bad-faith planning. That distinction is the heart of equity stripping architecture

💡 Core Idea: Equity stripping is not about hiding assets. It is about structuring legitimate financial obligations so visible equity is not left unnecessarily exposed to opportunistic claims

⚖️ What Is Equity Stripping?

Equity stripping is the process of reducing exposed equity in an asset by placing a valid financial obligation against it. In a real estate context, this may involve a mortgage, deed of trust, home equity line, commercial loan, or properly recorded lien. In a business context, it may involve secured financing against equipment, inventory, receivables, vehicles, or other corporate assets

The purpose is to make the asset less attractive as a litigation target. A plaintiff or judgment creditor usually wants recoverable value. If an asset is already heavily encumbered by legitimate senior debt, the available equity may be limited. This can reduce the incentive to spend money pursuing that asset

At an advanced level, equity stripping is less about one transaction and more about architecture. It requires careful coordination between entity structure, asset ownership, financing documents, lien recording, tax treatment, solvency, corporate governance, and litigation timing

🧠 Why Litigation Targets Visible Equity

Lawsuits are often driven by economics. A claimant, attorney, or creditor wants to know whether a target has collectible value. Visible equity sends a signal. A commercial building with little debt, a fleet of debt-free vehicles, or expensive equipment held by an operating company can make litigation more attractive

Predatory litigation thrives on leverage. If the opposing side sees clean assets, it may assume settlement pressure will be easier to create. Even weak claims can become expensive if the defendant appears financially exposed

Equity stripping changes the economics. When assets are already subject to legitimate senior claims, the expected recovery may look lower. That does not eliminate litigation risk, but it can reduce the attractiveness of a forced collection strategy

"Asset protection is not only about owning less. It is about exposing less collectible value to the wrong audience"

🏛️ Why This Belongs Under Institutional Risk

Institutional risk focuses on the systems that protect businesses, owners, investors, and private structures from legal, financial, operational, and reputational damage. Equity stripping belongs in this category because it directly affects how assets appear under legal pressure

A company may have strong operations, profitable contracts, and valuable assets, yet still be vulnerable if those assets are held in a way that invites creditor attention. Clean equity can be useful for borrowing, valuation, and balance sheet strength. However, it can also become a litigation magnet

The challenge is balance. Too much visible equity can create exposure. Too much artificial debt can create suspicion. A strong institutional-risk strategy avoids both extremes

🔐 The Difference Between Legitimate Encumbrance and Sham Debt

The success of equity stripping depends on legitimacy. A recorded lien is not automatically protective just because it appears in public records. Courts and creditors can look behind the paperwork to determine whether the obligation is real

A legitimate encumbrance normally has a real economic purpose, a documented loan agreement, fair consideration, commercially reasonable terms, proper recording, actual payment behavior, and consistency with tax and accounting records

A sham lien, by contrast, may involve no real debt, no payment history, no business purpose, no fair value, no independent documentation, or suspicious timing after a claim has arisen

⚠️ Important: A lien created merely to block an existing creditor may be challenged under fraudulent-transfer or voidable-transaction rules. Equity stripping should be planned in advance and reviewed by qualified legal counsel

📌 The Architecture of a Proper Equity-Stripping Strategy

Equity stripping architecture is not a quick fix. It is a layered planning model that must be integrated with the company's larger legal and financial structure

The architecture usually begins with identifying which assets carry the greatest exposure. These may include real estate owned by an operating company, equipment used in high-liability work, vehicles used in commercial activity, or valuable assets held in an entity that also signs customer contracts

Once exposure is identified, the company evaluates whether the asset should remain in the operating entity, be transferred to a holding entity, be leased back to operations, be financed through a commercial lender, or be subject to a legitimate secured obligation

Visible Asset

A property, vehicle, machine, or equipment portfolio with clear equity that may attract legal pressure.

Strategic Encumbrance

A valid lien, mortgage, or security interest that reduces exposed collectible equity

🏢 Corporate Real Estate and Equity Exposure

Corporate real estate is one of the most common assets involved in equity-stripping discussions. A company that owns warehouses, offices, rental property, development land, or commercial units may appear attractive to litigants if those properties have substantial equity

In many cases, the issue is not that the company owns real estate. The issue is that the real estate is held in the same entity that carries operational risk. If the operating company signs contracts, employs staff, manages customer disputes, owns vehicles, and holds real estate, then the property may be exposed to the same liabilities as the business operation

A stronger structure may separate the real estate from the operating company. The property-owning entity can lease the asset to the operating company under a formal lease. This creates operational separation. If appropriate, the property may also carry legitimate financing that reduces exposed equity

The result is not invisibility. The result is structured separation

⚙️ Equipment, Machinery, and Secured Financing

Equity stripping is not limited to real estate. Businesses with valuable equipment can also face exposure. Manufacturing companies, logistics firms, construction businesses, medical facilities, restaurants, and industrial operators may own expensive machinery that appears collectible

Equipment can be protected through legitimate secured financing, lease structures, equipment finance agreements, or ownership separation. For example, a separate equipment-holding entity may own machinery and lease it to the operating company. The equipment-holding entity may also finance the equipment through a lender with a recorded security interest

This type of structure must be documented carefully. Lease payments should be commercially reasonable. Ownership records should be consistent. Insurance should match the structure. Accounting treatment should not contradict the legal arrangement

🧩 Institutional Principle: A protective structure is strongest when legal documents, tax records, accounting records, insurance policies, and business behavior all tell the same story

🤝 Friendly Mortgages: Useful but Dangerous

A "friendly mortgage" generally refers to a mortgage, lien, or secured loan issued by a related party, friendly lender, family entity, trust, or closely connected business. The idea is to place a senior claim against an asset before hostile creditors appear

Friendly mortgages can be risky because courts may examine whether the loan is genuine. If the lender is closely related to the borrower, the transaction may receive extra scrutiny. The court may ask whether money actually changed hands, whether repayment was expected, whether interest was charged, whether payments were made, and whether the lender behaved like a real creditor

A friendly mortgage that exists only on paper may offer little protection. Worse, it may damage credibility and invite allegations of fraudulent transfer or sham transaction

What Makes a Friendly Mortgage More Defensible?

- ✅ A legitimate business or financing purpose

- ✅ Real consideration or actual value exchanged

- ✅ Written loan documents prepared before trouble arises

- ✅ Commercially reasonable interest and repayment terms

- ✅ Proper recording of the lien or mortgage

- ✅ Consistent payment history

- ✅ Accurate tax and accounting treatment

- ✅ No intent to defeat a known creditor claim

🚫 The Fraudulent Transfer Problem

The biggest danger in equity stripping is the fraudulent transfer problem. Despite the name, modern voidable-transaction law does not always require dramatic fraud. A transfer or obligation can become vulnerable if it is created with improper intent or if it leaves the debtor unable to meet obligations while not receiving reasonably equivalent value

This is why timing matters. Equity stripping performed long before any dispute, lawsuit, demand letter, or creditor problem is usually easier to defend than a rushed encumbrance created after trouble begins

Courts may examine badges of fraud. These can include insider transactions, lack of fair value, secrecy, insolvency, unusual timing, retention of control, or transactions made shortly before or after a creditor claim appears

⚠️ Red Flag: If an entity creates a lien after receiving a lawsuit threat, demand letter, tax claim, judgment, or creditor pressure, the transaction may be challenged and potentially unwound

📊 Equity Stripping vs. Asset Hiding

A responsible strategy must clearly separate equity stripping from asset hiding. Asset hiding implies concealment, deception, or misleading creditors. Equity stripping, when done legitimately, involves real transactions, recorded interests, valid obligations, and transparent documentation

The objective is not to lie about asset ownership. The objective is to avoid leaving excessive unprotected equity exposed in a way that encourages predatory litigation

This difference matters because courts, banks, insurers, and counterparties care about intent. A structure designed for real financing, operational separation, estate planning, or risk allocation is very different from a fake lien created solely to block collection

🧾 Documentation: The Real Backbone of the Strategy

Documentation is the difference between a protective architecture and a fragile paper shield. Every equity-stripping structure should be supported by a formal compliance file

This file should include loan agreements, promissory notes, security agreements, mortgage documents, board approvals, valuation records, payment records, banking evidence, tax treatment notes, insurance records, lease agreements, and legal review memos

The documentation should show that the transaction was real, commercially understandable, and created for a legitimate purpose

- 📄 Promissory note or loan agreement

- 🏛️ Mortgage, deed of trust, or security agreement

- 📌 Proper public recording or UCC filing where applicable

- 💰 Evidence of funds advanced or value exchanged

- 📆 Payment schedule and payment history

- 🧾 Accounting and tax treatment

- 🛡️ Insurance and ownership records

- ⚖️ Legal review and governance approvals

🏦 Commercial Lenders vs. Friendly Lenders

Commercial lenders are often easier to defend because the transaction is arm's length. A bank, credit union, private lender, or equipment-finance company typically has underwriting standards, real documentation, repayment expectations, and independent economic motivation

Friendly lenders can still be legitimate, but they require stronger discipline. Related-party transactions should be treated as seriously as third-party transactions. The lender should behave like a lender. The borrower should behave like a borrower. Payments should be made. Defaults should have consequences. Records should be maintained

If the friendly lender would never enforce the debt, never demand repayment, and never act independently, the structure may look weak

🧱 Pairing Equity Stripping With Entity Separation

Equity stripping is rarely strongest as a standalone strategy. It works best when paired with entity separation

Entity separation means valuable assets are not unnecessarily held inside high-risk operating companies. Instead, real estate may be held by a property company. Equipment may be held by an equipment company. Intellectual property may be held by an IP holding company. The operating company then leases or licenses what it needs

This approach creates legal and operational boundaries. If the operating company faces a claim, the claimant may have a harder time reaching assets held in separate entities, assuming the structure is properly maintained and not abused

Corporate formalities matter. Separate bank accounts, separate records, written agreements, fair-market payments, and proper accounting are essential

🌍 Jurisdictional Arbitrage and Recorded Liens

Jurisdictional arbitrage plays an important role in equity stripping. Different jurisdictions have different rules for recording liens, enforcing judgments, protecting LLC interests, recognizing security interests, and analyzing fraudulent transfers

A sophisticated structure should consider where the asset is located, where the entity is formed, where the company operates, where litigation is likely to occur, and how creditors may enforce claims

For real estate, local law generally matters because property is tied to its physical location. For equipment and movable assets, secured transaction rules and filing systems may become important. For membership interests in LLCs, charging-order protections and state entity law may matter

🌎 Advanced Planning Note: Jurisdictional arbitrage is not about choosing the most secretive location. It is about selecting the most defensible legal environment for the asset, entity, transaction, and risk profile

📉 Solvency: The Test Many People Ignore

Solvency is a critical issue in equity-stripping analysis. If a company encumbers assets so heavily that it cannot meet its obligations, the transaction may become vulnerable

A responsible structure should preserve operational solvency. The company should still be able to pay ordinary debts, taxes, employees, vendors, lenders, and operating expenses. If a transaction leaves the company unable to function, it may look like an attempt to defeat creditors rather than a legitimate financing decision

Advanced planning often includes solvency analysis, cash-flow forecasting, asset valuation, and board-level approval. These records can help demonstrate that the transaction had a legitimate purpose and did not leave the entity financially impaired

🛡️ Insurance Still Matters

Equity stripping should never be treated as a replacement for insurance. Insurance remains the first line of defense against many business risks

General liability insurance, professional liability coverage, umbrella coverage, property insurance, workers' compensation, cyber insurance, directors and officers coverage, and commercial auto policies may all play a role depending on the business

A mature institutional-risk strategy combines insurance, entity separation, contract drafting, operational controls, compliance systems, and asset-encumbrance planning. No single technique should carry the entire burden

🔎 Common Mistakes in Equity Stripping

Many equity-stripping strategies fail because they are rushed, artificial, or poorly maintained. The most common mistake is waiting until a claim appears. Once a business is already facing litigation, tax pressure, creditor demands, or regulatory action, major asset transfers and new liens become far more suspicious

Another mistake is creating debt with no real economic substance. A promissory note that is never paid, a mortgage that is never enforced, or a lien that has no supporting loan may be vulnerable

Businesses also make mistakes by ignoring tax treatment, failing to record documents properly, using informal family arrangements, mixing entity funds, or failing to keep corporate records updated

- 🚫 Creating liens after litigation starts

- 🚫 Using fake loans with no funds advanced

- 🚫 Failing to make payments

- 🚫 Ignoring tax and accounting consistency

- 🚫 Mixing personal and business assets

- 🚫 Leaving operating companies with valuable unprotected assets

- 🚫 Treating related-party loans casually

- 🚫 Forgetting insurance and contract risk controls

🧩 A Clean Framework for Institutional Operators

A clean equity-stripping framework begins with a risk audit. The company identifies visible assets, estimates exposed equity, reviews current ownership, and evaluates existing liabilities

Next, the company reviews whether each asset belongs in its current entity. If the operating company owns valuable real estate, equipment, or intellectual property, the structure may need to be reconsidered with professional advice

Then, the company evaluates legitimate financing options. These may include commercial loans, equipment financing, refinancing, secured lines of credit, lease structures, or related-party financing with formal documentation

Finally, the company creates a monitoring system. Asset values change. Debt balances change. Litigation risk changes. Entity operations change. A structure that made sense five years ago may need adjustment today

✅ Equity Stripping Architecture Checklist

- ✅ Identify high-value visible assets

- ✅ Separate operating risk from asset ownership where appropriate

- ✅ Use legitimate financing, not artificial paper debt

- ✅ Record liens, mortgages, or security interests correctly

- ✅ Maintain payment records and financial consistency

- ✅ Review solvency before and after major transactions

- ✅ Avoid rushed planning after creditor claims arise

- ✅ Treat friendly loans as real loans

- ✅ Align legal records with accounting, tax, and insurance records

- ✅ Combine equity stripping with insurance and contract protection

- ✅ Revisit the structure after major asset or business changes

- ✅ Use qualified legal and tax professionals before implementation

🏁 Conclusion: Encumbrance Is Not Evasion

Equity stripping can be a powerful concept in institutional risk architecture, but only when it is designed with discipline. The objective is not to deceive creditors, hide assets, or create false paperwork. The objective is to avoid leaving excessive collectible equity exposed in a way that invites predatory litigation

The best structures are built early, documented carefully, supported by real economics, and integrated with broader asset-protection planning. They use legitimate debt, proper recording, entity separation, insurance coverage, and governance discipline

The weakest structures are rushed, informal, related-party arrangements with no real substance. These may collapse under scrutiny and create greater risk than they solve

For sophisticated operators, the lesson is clear: visible equity must be managed like any other institutional exposure. Real estate, machinery, and corporate assets should not sit unprotected inside risky operating environments. They should be structured, financed, documented, and monitored with precision

"In advanced asset protection, the safest equity is not hidden equity. It is disciplined equity, structured before conflict and supported by real documentation"

About The Author

Mubeen Aslam writes about capital intelligence, risk management, economic analysis, compliance, and institutional resilience. His work focuses on explaining complex risk concepts in clear, educational language for business owners, founders, and readers studying long-term capital protection.

View all articlesExplore More

Continue Reading

Related Articles

Stay Ahead

Love this article?

Join our newsletter to get more articles like this delivered straight to your inbox. No spam, just value

Enter your email to download

We will use this email to record and deliver your requested resource.

Comments